Major Credit Card Company - Transaction Risk Monitoring

Fabric Score 3.9

PrivateFinanceMajor Credit Card CompanyNon-GenAI modelExecutive / Org Leadership ×1

Workflow Diagram

Fabric Score

Task

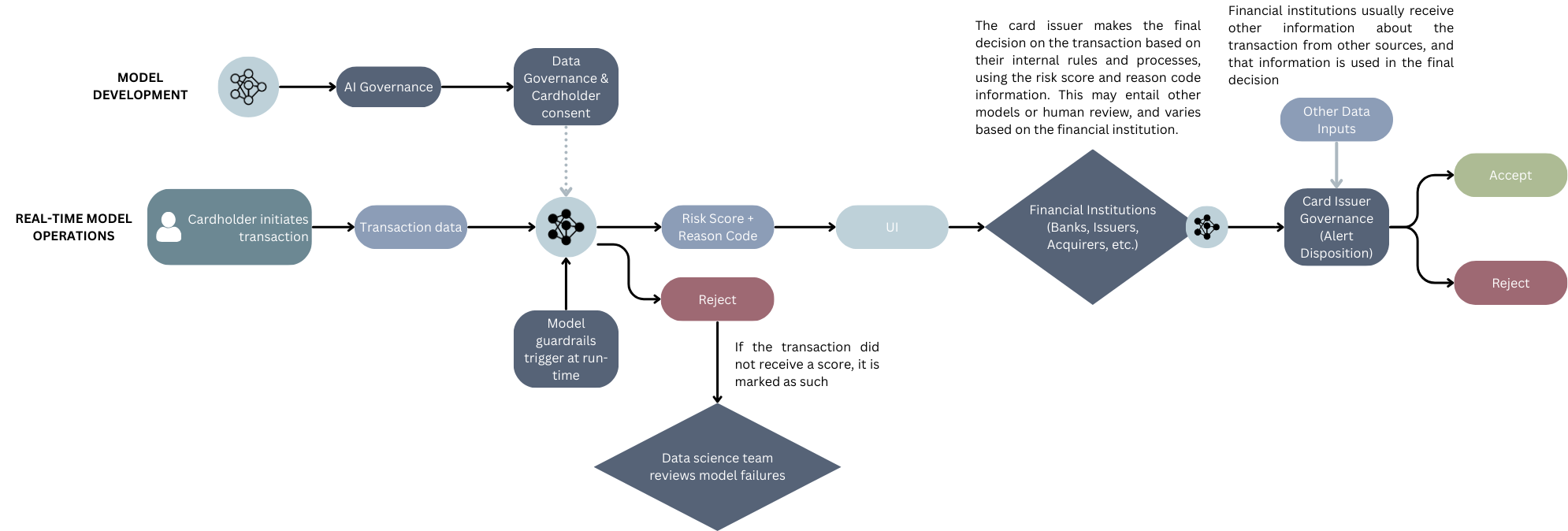

When a card is used for an in-person transaction, the model generates a risk score for how risky that transaction is. That score is sent to card issuers (banks), and the issuers use the score to make a decision on accepting or rejection the transaction.

Intent

The AI system provides granular risk scores for in-person transaction.

AI Workflow

Input

Card holder uses their credit card at a merchant to make a transaction, a set of data about that transaction is sent to the fraud model.

Process

The AI system generates a risk score for the transaction, which is sent to the financial institutions who make the ultimate decision about whether to accept or reject that transaction.

Output

Output of the fraud model itself is a risk score that is used by the card issuer. The ultimate output is a decision to reject or accept the transaction, which is made by the financial institutions involved.

Human Oversight Level

Conditionally Autonomous AI

Institutional Oversight Examples

- •AI Governance oversees and reviews models

- •Product models are developed and overseen by the data scientists

- •Financial Institutions are governed by a number of regulatory and legal obligations for payments (SR 11-7, FRB, OCC & FDIC regulations in the US)

- •ISO 8583 & ISO 20022

Risk

Transactions could be rejected when they are actually valid, losing customers and trust.

Output Modification Telemetry

- Other100%

Transversal Metrics

Grouped by Fabric dimension.

Efficacy

Accuracy90 %

Efficiency

Operational Friction200 hrs/wk

Implementation Overhead20 hrs

Time to Launch20 wks

Value

Effort Reduction99 %

Effort BurdenN/A (information varies)

Risk

ReliabilityN/A